This initial check-up is essential for an accurate balance sheet and income statement later on. If totals are not equal, it means that an error was made in the recording and/or posting process and should be investigated. In other words, a trial balance shows a summary of how much Cash, Accounts Receivable, Supplies, and all other accounts the company has after the posting process.

How to prepare an unadjusted trial balance

An adjusted trial balance is a listing of the ending balances in all accounts after adjusting entries have been prepared. Unadjusted trial balance is an important step towards preparing a complete set of financial statements. ¹ You will get an overview of all the accounts that are used in your business for example, sales account, purchase account, inventory account etc. in a summary form with the help of an unadjusted trial balance. The unadjusted trial balance is prepared to check if all accounts have balances. It helps ensure that all transactions for a given period are accounted for before adjusting entries are made. A trial balance is an accounting report that lists the ending balances of general ledger accounts to ensure the debit and credit balances are equal.

- These fine-tunings help present a true financial position before final reports are prepared.

- Once all adjustments are made to the unadjusted trial balance, we will have the adjusted trial balance.

- If they aren’t equal, the trial balance was prepared incorrectly or the journal entries weren’t transferred to the ledger accounts accurately.

- Making sure these numbers are right is super important for the financial statement to be correct.

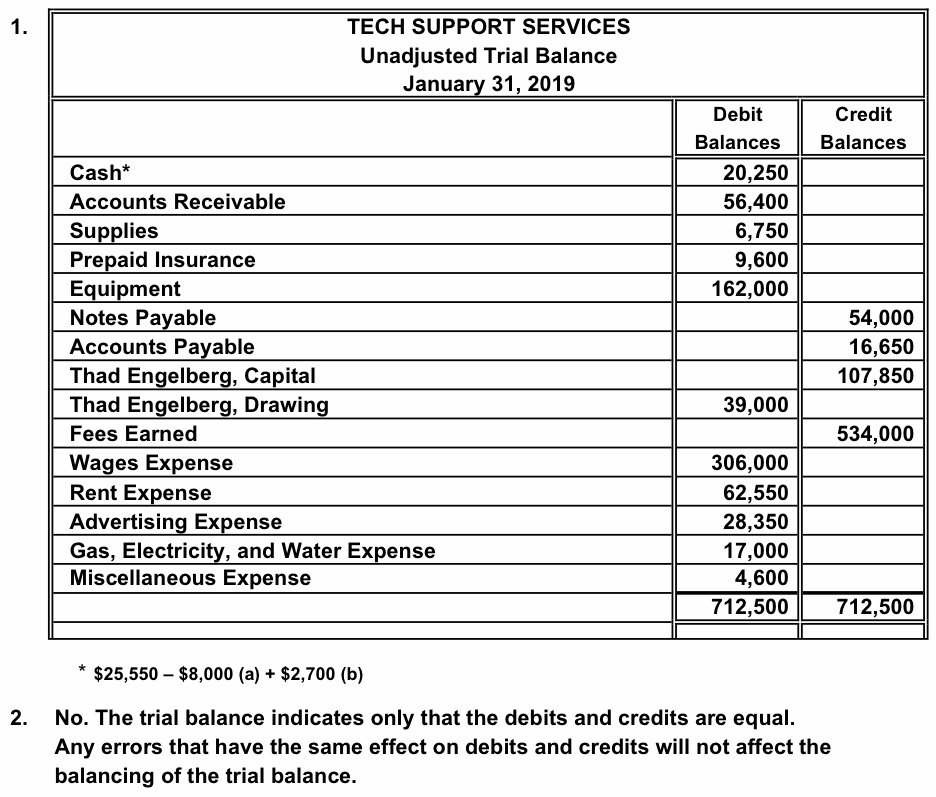

Equal Doesn’t Always Mean Correct

Several reasons require an accountant to adjust the company’s accounting ledgers. The name “unadjusted” implies that no adjustment has been made to the accounts or their balances and reflects the basic financial information for a certain period. Since most companies have computerized accounting systems, they rarely manually create a TB or have to check for out-of-balance errors. In case of errors, simply edit the 1st and 2nd columns of UBTB until you get the correct balances.

Step 3 of 3

At the end of the accounting period, the accountant prepares a trial balance from the account information contained in the general ledger. This trial balance lists most of the assets, liabilities, revenues, and expenses of the business, but these amounts are incomplete because adjusting entries have not yet been prepared. Therefore, this trial balance what is a single step income statement is called an unadjusted trial balance. This step saves a lot time for accountants during the financial statement preparation process because they don’t have to worry about the balance sheet and income statement being off due to an out-of-balance error. Keep in mind, this does not ensure that all journal entries were recorded accurately.

Which of these is most important for your financial advisor to have?

Accountants create an unadjusted trial balance to check if the total debits equal the total credits, which shows whether the books are in basic balance. Understanding these distinctions is imperative for professionals in the field of accounting. Accurate preparation and analysis of unadjusted and adjusted trial balances ensure the integrity of a company’s financial reporting. Unadjusted trial balance is used to identify the necessary adjusting entries to be made at the end of the year.² Adjusting entries are made mainly due to the usage of accrual system of accounting.

Would you prefer to work with a financial professional remotely or in-person?

Now, most companies use an accounting system where the system automatically creates the trial balance. Not all accounts in the chart of accounts are included on the TB, however. Usually only active accounts with year-end balance are included in the TB because accounts with zero balances don’t make it on the financial statements. For example, if a company had a vehicle at the beginning of the year and sold it before year-end, the vehicle account would not show up on the year-end report because it’s not an active account.

Find an example balance sheet and use our free balance sheet template to review your company’s financial position. After the preparation of an unadjusted trial balance, the next step in the accounting cycle is to pass adjusting entries. The trial balance is used to test the equality between total debits and total credits. For example, adjustment to correct over accrual of electricity expenses. Or correcting adjustments when the accountant noted that the debit balance and credit balance of the trial balance are not reconciled due to the incorrect entries made into the general ledgers.

An unadjusted trial balance is a trial balance which is created before any adjusting entries are made in the ledger accounts. A Trial Balance is a list of all the accounts of a business and their balances; its purpose is to verify that total debits equal total credits. When the accounting system creates the initial report, it is considered an unadjusted trial balance because no adjustments have been made to the chart of accounts. This is simply a list of all the account balances straight out of the accounting system. If a company creates financial statements on a monthly basis, the accountant would print an unadjusted trial balance at the end of each month to initiate the process of creating financial statements.